Still Exploring?

Looks like you’ve been exploring our platform.

Want to see everything in one place?

The CSRD is part of the European Green Deal, which is a set of policies and initiatives aimed at making Europe the first climate-neutral continent by 2050. When it first came into effect, the CSRD expanded the scope of environmental, social, and governance (ESG) reporting requirements. It also required independent third-party audits of companies’ sustainability reports to ensure that the information is accurate and reliable.

However, on February 26, 2025, the European Commission published proposals for the first Omnibus Simplification Package. The proposals outline amendments to the CSRD, among other EU regulations, that reduce the regulation scope and timelines and removes a number of other requirements.

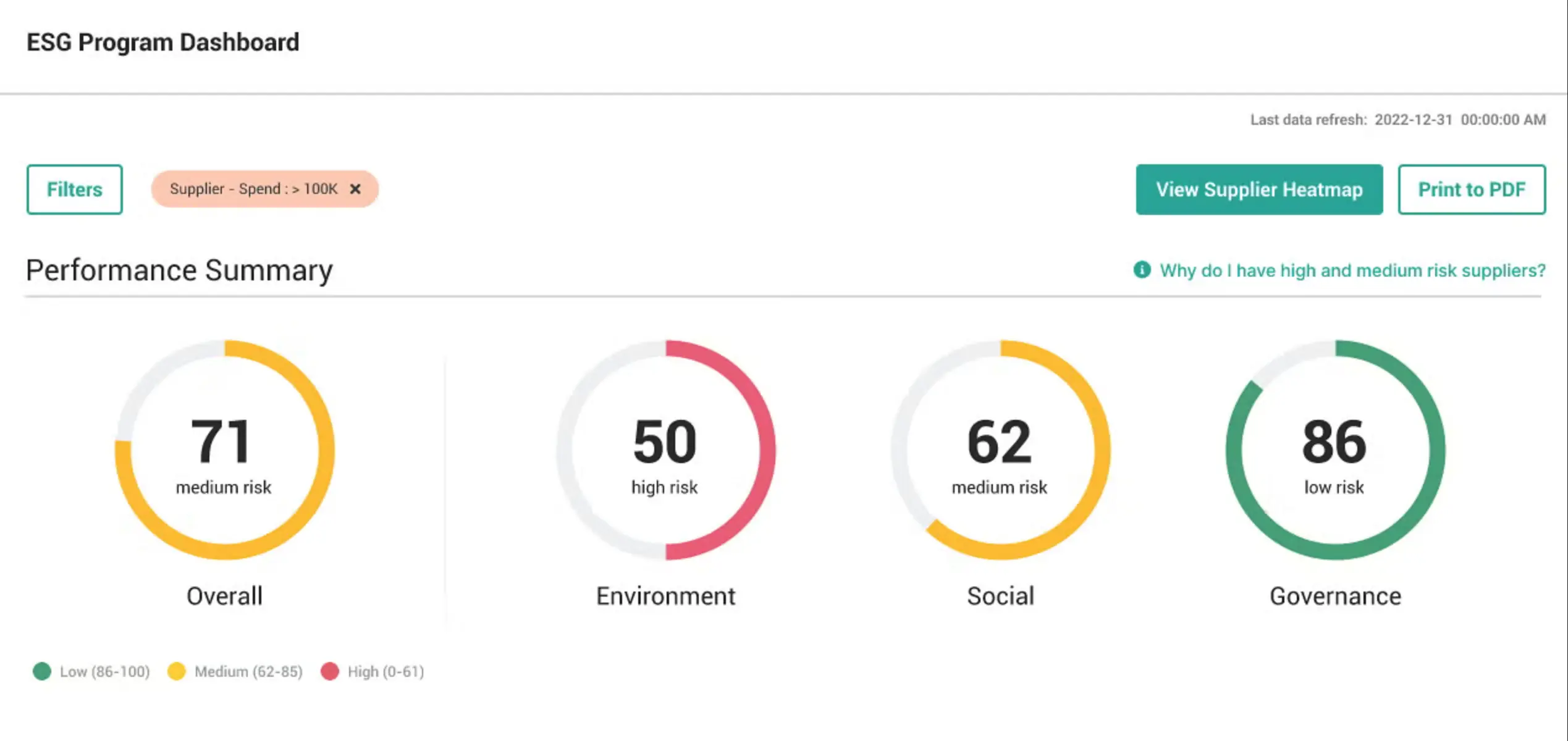

The CSRD marks a new era of non-financial reporting requirements due to rising ESG demands. Requiring standardized reporting to enable more informed investment decisions, the CSRD will significantly impact corporate sustainability reporting in the EU and have an extended ripple effect around the world. These impacts include:

Need help navigating your requirements? Check out our latest resources and product tour.

Under the EU Corporate Reporting Sustainability Directive (CRSD) manufacturers face new ESG reporting requirements.

Assent’s ESG solution offers comprehensive support for all your ESG requirements. Explore our solution and feature capabilities to see why complex manufacture …

Learn how to source defensible product, regulatory compliance, and supply chain data with insights from product sustainability experts.